The Price of Oil, by Roberto Aguilera and Marian Radetzki – Part 1

Published by Angharad Lock,

Digital Assistant Editor

World Pipelines,

The following is Part 1 of a press release covering The Price of Oil, by Roberto Aguilera and Marian Radetzki.

The Price of Oil, by Roberto Aguilera and Marian Radetzki, is to be published by Cambridge University Press in November 2015. Aguilera and Radetzki argue that although oil has experienced an extraordinary price increase over the past few decades, a turning point has now been reached where scarcity, uncertain supply and high prices will be replaced by abundance, undisturbed availability and suppressed price levels in the decades to come.

Aguilera and Radetzki examine the implications of this turnaround for the world economy, as well as for politics, diplomacy, military interventions and the efforts to stabilise climate.

Below is a brief chapter-by-chapter summary of The Price of Oil.

Part: Oil’s extraordinary price history

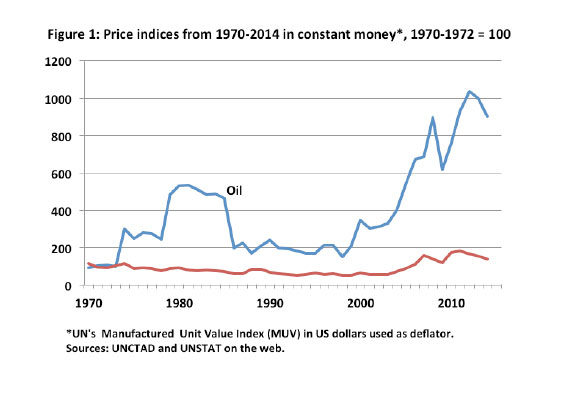

Oil price developments over the past 40 years have been truly spectacular. In constant money, prices rose by almost 900% between 1970-72 and 2011-13 (Figure 1). This can be compared with a 68% real increase for a metals and minerals price index, comprising a commodity group, which like oil belongs to the exhaustible category. The objective of this part is to explain the price exceptionality of oil.

Aguilera and Radetzki do not share the widespread opinion that OPEC’s interventions since the early 1970s have had a major influence on the price behavior of oil. They argue, that while OPEC cooperation has undoubtedly had short-term impacts on the oil market, its interventions are completely inadequate for explaining the longer run price performance. Underlying Aguilera and Radetzki’s position is a number of academic studies pointing to the short run and insubstantial nature of the oil group’s supply-restraining actions. However, it needs mentioning that actions of Saudi Arabia in isolation to limit output, and even more, the country’s cautious approach to capacity expansion, have clearly contributed to the oil price evolution.

Instead, Aguilera and Radetzki argue that a number of political rather than economic forces have shaped the inadequate growth of upstream production capacity, the dominant factor behind the long run upward price push. This is particularly, but not exclusively, true in OPEC, the country group with a leading share of global oil reserves.

Widespread nationalisations of the oil sector in the 1970s replaced private multinationals with state owned enterprises. The latter did not invest much in capacity expansion because of a persevering lack of technical proficiency in many cases and a tendency of their government owners to use the surpluses generated by oil production in support of the state budget, so leaving insufficient resources for investment. A variety of goals apart from profit were often imposed on the state owned firms, resulting in high costs and inefficiencies that further reduced investments in new capacity.

Private multinationals had been deprived of a sizable proportion of conventional oil reserves in the nationalisation wave, so they could not easily compensate for the state owned deficiencies in capacity expansion. Furthermore, as prices and profits rose in consequence of rising demand and stagnant production capacity, virtually all producing governments, inside and outside OPEC, sharply raised taxes and other impositions, further reducing the willingness to invest. In this way, a vicious circle was put in place, and its operation was made viable by the very low price elasticity of demand (i.e. unresponsive demand to even significant price changes) in the short- and medium-term.

While some believe that depletion and thus rising costs can explain price developments, the continuous rise of global oil reserves along with the high level of pre-tax profits in the industry are clear indicators that depletion has not been a factor behind the observed oil price evolution.

The resource curse, represented by domestic and international conflicts over the oil rent, is probably the most important explanation to the extraordinary oil price developments. Aguilera and Radetzki have looked at only six countries – Iran, Iraq, Libya, Nigeria, Sudan and Venezuela, all richly endowed with oil resources – to conclude that the resource curse had suppressed their recent production levels below peaks attained decades ago by a total of 7 million bpd, corresponding to no less than 55% of overall annual oil consumption in the European Union. In the absence of such suppression, oil prices would clearly have been far below the heights seen between the end of 2010 and autumn 2014.

Part: The shale and conventional oil revolutions

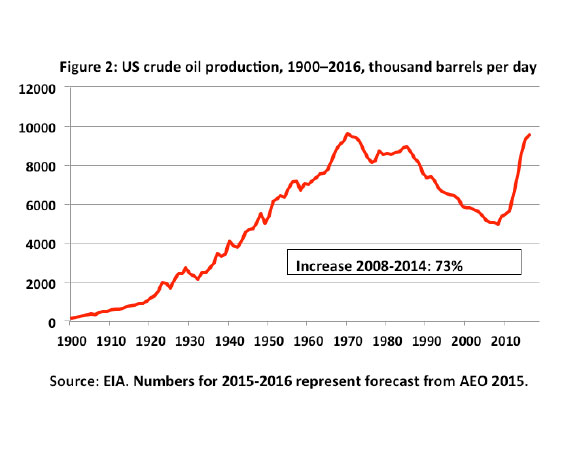

The shale oil revolution has unexpectedly and forcefully begun to transform the energy landscape in the US. Beginning less than 10 years ago, the revolution – employing technological innovations in horizontal drilling and hydraulic fracturing – has turned the long run declining oil production trends in the US into rises of 73% between 2008 and 2014 (Figure 2). The shale oil costs become broadly competitive at oil prices of US$50 per barrel, lower than the costs of Canadian oil sands and Brazilian deep offshore pre-salts. An exceedingly high rate of productivity improvements in this relatively new industry promises to strengthen the competitiveness of shale output even further. The revolution has had a number of positive effects for the US economy in terms of, for example, investments, employment, fiscal revenue and a strengthening trade balance.

The US lead in the shale revolution has many explanations, including large-scale and long-lasting conventional oil exploitation, a well-developed fossil fuel infrastructure, established production of inputs, many small adventurous prospecting and production enterprises, a relatively sympathetic public approach to the new industry, and the incentive to the landholder of underground resources ownership.

A series of environmental problems related to shale exploitation have been identified, most of which are likely to be successfully handled as the infant, ‘wild west’ industry matures and as environmental regulation is introduced and sharpened.

Geologically, the US does not stand out in terms of shale resources. A very incomplete global mapping suggests a US shale oil share of no more than 17% of a huge geological wealth widely geographically spread, with lead positions held by countries like Argentina, Australia, Mexico, China, Libya and Russia. Given the mainly non-proprietary shale technology and the many advantages accruing to the producing nations, it is inevitable that the revolution will spread beyond the US.

Aguilera and Radetzki have assessed the prospects of non-US shale oil output in 2035, positing that the rest of the world will by then exploit its shale resources as successfully as the US has done in the revolution’s first ten years – implying that the global revolution will occur with a substantial delay and at a much slower pace than the one achieved by the US. With roughly a 17% share of global shale resources, the US in 10 years expanded its output by 3.9 million bpd. Assume, then, that the rest of the world is equally as successful as the US was between 2004-2014 in exploiting its share of the resources between 2015-2035. This would yield rest of world output of 19.5 million bpd in 2035 (Table 1), which is similar to the global rise of all oil production in the preceding 20 years – a stunning deduction with far-reaching implications in many fields.

| Table 1: Speculative ROW shale oil impact to 2035, million bpd | ||||

|---|---|---|---|---|

| Global 2014 oil output | Global rise, 20 years (1994 - 2014) | US share of shale oil resources, EIA (2013a) | US shale production rise, 10 years (2004 - 2014) | ROW shale production rise, 20 years (2015 - 2035) |

| 88.7 | 21.6 | 17% | 3.9 | 19.5 |

Part 2 is available here.

Edited from press release by Angharad Lock

Read the article online at: https://www.worldpipelines.com/special-reports/21092015/the-price-of-oil-by-roberto-aguilera-and-marian-radetzki-part-1/

You might also like

The World Pipelines Podcast

A podcast series for energy professionals featuring short, insightful interviews with experts who can shed light on topics that matter to you and your business. Subscribe on your favourite podcast app to start listening today.

![]()

![]()

![]()

![]()