Morningstar DBRS: Crude oil prices surge on Gulf conflict, but long-term trajectory is still unclear

Published by Elizabeth Corner,

Senior Editor

World Pipelines,

Crude oil prices have increased sharply since the United States and Israel started their coordinated strikes on Iranian military targets on 28 February 2026. Iran countered, launching missiles and drones at US bases and regional allies. The higher crude prices reflect the increased political risk premium and potential disruption in supply as maritime authorities and carriers, in response to the conflict, have halted traffic through the Strait of Hormuz (the Strait), which sees roughly 20% each of global crude oil and seaborne gas flows.

It is unclear at this time whether the price increase is sustainable over the medium term because the conflict is still in its early stages, and it is difficult to determine if there will be structural impact on oil and gas supply coming out of the region. The crude markets have already been grappling with the question of whether there is a supply glut coming in 2026, and the conflict, along with OPEC+'s 1 March 2026, announcement to increase production (albeit not materially), only makes things murkier. Our previous report from January 2026 (2026 Oil and Gas Outlook: Geopolitical Risk Could Upend Expectations for Crude Surplus; Cold Wave Boosts Gas Prices) stated we expected West Texas Intermediate (WTI) and Brent crude oil prices to average $US60/bbl and US$63/bbl, respectively, in 2026. Given the uncertainty, we are not changing our base-case price assumptions at this time; however, events are unfolding quickly and we will continue to monitor geopolitical developments and assess whether we need to adjust our price forecasts. Based on year-to-date prices and near-term expectations, there is potential upside to our full-year 2026 Brent and WTI crude oil price forecasts.

Disruptions in the Strait remain a key concern

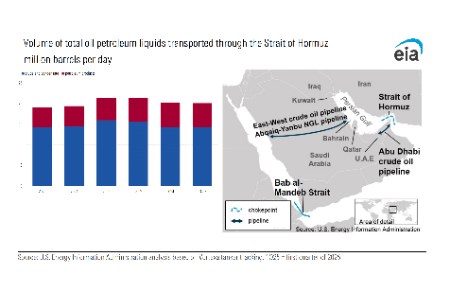

Approximately 20 million bpd of crude oil and petroleum products flow through the Strait, located between Oman and Iran, connecting the Persian Gulf with the Gulf of Oman and the open sea (see image). It is one of the world's most important oil choke points. Production from some of the world's largest crude oil producers, such as Saudi Arabia, Iraq, Iran, United Arab Emirates, and Kuwait, are partially routed through the Strait. While there is some overland access for crude oil out of the region, it is nowhere near sufficient to replace flows through the Strait. In addition, Qatar, which is one of the largest exporters of liquified natural gas (LNG) to the world, routes all its LNG shipments through the Strait with no viable alternative options. Qatar has already shut down its largest LNG plant because of a targeted drone attack. Any sustained disruption in LNG supply from Qatar could potentially boost delivered natural gas prices. Qatar is one of the largest LNG suppliers to Asia, and the disruption will come at a time when European natural gas storage levels are also at their lowest level since 2022 because of a harsh winter. This could create a surge in demand for LNG cargo from other countries including the United States, which is the world's largest LNG exporter, driving New York Mercantile Exchange gas prices higher.

Loss of supply from Iran a lesser concern

Iran produces approximately 3 million bpd of crude oil and, at the time of publishing, there have been no reports of attacks on Iran's oil infrastructure. Nevertheless, we expect the impact of any loss of potential production from Iran to have a lesser impact on crude oil prices compared with the closure of the Strait. In our 2026 outlook, we had outlined our view that the crude oil markets will be in a surplus in the first half of 2026 and that should provide a buffer for any loss of production from Iran. In addition, eight OPEC+ countries announced on 1 March 2026, that they would resume unwinding the 1.65 million bpd of voluntary cuts announced in April 2023 with an increase of 206 000 bpd in April 2026. Also, OPEC+ has an additional 2.2 million bpd of voluntary cuts announced in November 2023 that have yet to be unwound. While some of that capacity may only exist on paper, it is still significant spare capacity. Many US producers have been cautious on growing production because of worries about a negative tariff-related effect on the global economy, and oil demand growth could also step in quickly if WTI remains higher consistently.

Credit rating implications

Confidently projecting the direction of oil and natural gas pricing is a challenge, especially considering the potential for turbulence in both markets, and the conflict only makes it more so. We believe there is too much uncertainty to determine if crude oil prices will remain high, and it is largely dependent on how the conflict plays out. As such, there is no change to our midcycle pricing assumptions, so we are not currently contemplating any credit rating actions.

That said, in the short term, the increase in crude oil prices is modestly credit positive for the industry. Where applicable, higher cash flows should enable producers to achieve their deleveraging goals quicker. Producers that hedge material amounts of their production will also likely see windows of opportunity to beef up their hedge books.

Read the article online at: https://www.worldpipelines.com/business-news/03032026/morningstar-dbrs-crude-oil-prices-surge-on-gulf-conflict-but-long-term-trajectory-is-still-unclear/

You might also like

The World Pipelines Podcast

A podcast series for energy professionals featuring short, insightful interviews with experts who can shed light on topics that matter to you and your business. Subscribe on your favourite podcast app to start listening today.

![]()

![]()

![]()

![]()